Why Invest? Why not keep a bunch of cash under a mattress?

The simple answer, money that you do not invest will lose purchasing power over time. In other words, if you do not grow your money it will become worth less the longer you hold it.

So, how do you prevent your money from not only losing value but also growing it to open additional opportunities over time? Well, there are literally 1000’s of ways to have your money start working for you. Stocks, bonds, property, BDC’s, Bitcoin, SS, Startups, Collector’s art, annuities, and the list goes on. Some are easy to get started and others are extremely complicated.

Because the list so long, it can be overwhelming and hard to know where to begin to start investing your money. The basis of this post is to show you why you need to invest and how to start with the most common way via stocks.

Once you have a solid foundation, understand risk, and know how to protect your principle, then feel free to branch out into other investment opportunities you have a passion for.

Let’s get started with some of the reasons why you need investments to build wealth.

Keep More of Your Money

The more money you save the more you can invest to open opportunities Read this post to compliment your investing.

Why Investments and Not Cash or Simple Savings?

Over time there is something that works against your savings. We all know it, experience it every day, and know it’s impact.

It is inflation. What you might not know however, is how much it can impact your savings.

First What is Inflation?

Inflation is the rate at which the general level of prices for goods and services is rising and, consequently, the purchasing power of currency is falling.

Some Key Points about inflation from Investopedia

-

Inflation is classified into three types: Demand-Pull inflation, Cost-Push inflation, and Built-In inflation.

-

The most commonly used inflation indexes are the Consumer Price Index (CPI) and the Wholesale Price Index (WPI).

-

Inflation can be viewed positively or negatively depending on the individual viewpoint.

-

Those with tangible assets, like property or stocked commodities, may like to see some inflation as that raises the value of their assets.

-

People holding cash may not like inflation, as it erodes the value of their cash holdings.

-

Ideally, an optimum level of inflation is required to promote spending to a certain extent instead of saving, thereby nurturing economic growth.

Here is what inflation has done to a simple cup of coffee

:max_bytes(150000):strip_icc():format(webp)/inflation_color2-216537dd3aeb4365b991b67790765e4f.png)

Cash Vs. Inflation

Today’s money is tomorrow’s money, but tomorrow it will be worth less. In other words if you hold $5,000 in cash for 10 years, you will still have $5,000 in cash, but goods and services will have risen in price so your money does not buy as much as it did when 10-years ago.

How big is the impact? If the annual inflation over the 10-year period is 2%, that means your $5,000 is worth approximately $4,000 in ten years (or a loss of $1,000).

Bank Savings Vs. Inflation

At the saving rates offered by most banks today, the savings rate does not outpace inflation and therefore you are losing money each year in terms of purchasing power. In high-interest rate periods, the basic saving rate would almost certainly outpace inflation.

If the savings rate was 6% and inflation 2%, you would have a net savings rate of 4%.

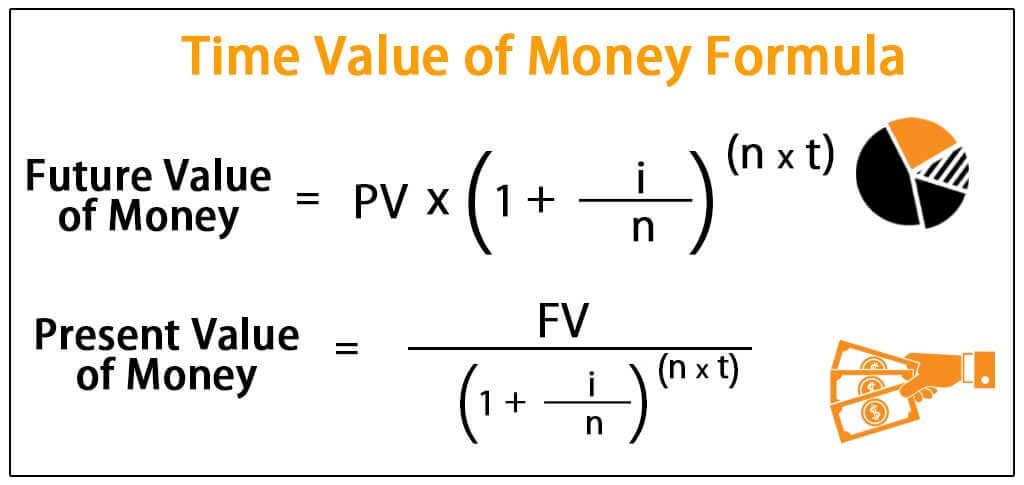

If you inclined to do so, here is the formula to calculate the time value of money based on certain assumptions (see examples of how to use the formula here). Kind of complicated, but really cool results. Fortunately, you don’t need to be a math wiz to understand the basic concept. If inflation is at 1.6%, you need a 1.6% return to stay even. It is that simple. Anything above that return and you are adding future vale to your investment.

Curious about the past value of dollars vs. today? I found this really cool inflation calculator to play around with. I like to see how much the value of a dollar has changed from when I was born to today.

When I put in my numbers, something that cost $1 when I was born now costs over $4.5. Wow. Something to think about, if everyone were given a $1,000 investment on their birth, a simple 6% return over 20 years would give everyone over $3,000 today on their 20th birthday.

Take it one step further, contribute $25 per month of savings for that same period and everyone would have almost $15,000 saved by the time they reach 20 which is more than most Americans have saved today across all ages.

What is $25, five cups of coffee, two days per month not eating out, 8 gallons of gas used. Not to much.

$1,000 invested at birth plus $25 a month to get $15,000 by age 20!

Investment Objective

The money you invest at a minimum should try to outpace inflation. Any investment that does not outpace inflation will lose purchasing power over time.

Beginning To Invest: Ideas to get started

Great, now that you know your first basic investment objective, let’s look at some begining investment types that are easy to get started.

Stocks, Mutual Funds, and Index Funds

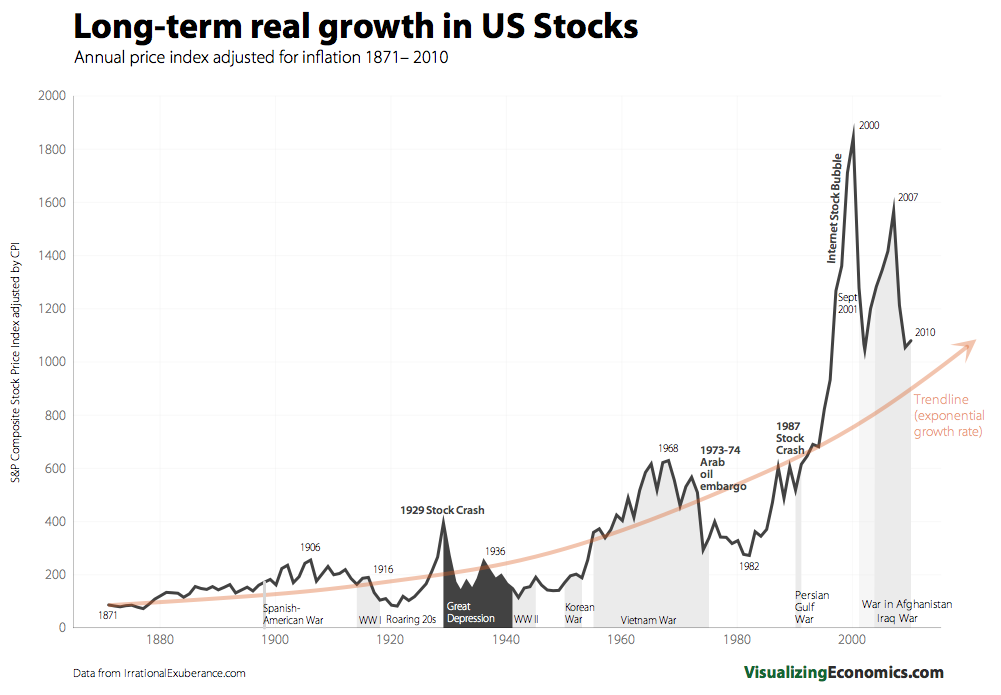

Remember our first investment objective – outpace inflation. The average returns for the market based on the S&P 500 is almost exactly 10% (before inflation).

That is pretty good considering average inflation is around 1.5-2%. As illustrated from the graph above, there is a lot of variabilities depending on world events, but over time the stock market has been consistently going up.

So what kind of options do you have to begin investing in the stock market?

Individual stocks are one such way to invest. Investing in an individual stock gives you the most flexibility to choose how, when, and what you invest in. With flexibility also comes greater risk and less diversification. Picking individual stocks can be difficult but can lead to great returns or great losses.

Understanding Stocks From Investopedia

Corporations issue (sell) stock to raise funds to operate their businesses. The holder of stock (a shareholder) has now bought a piece of the corporation and has a claim to a part of its assets and earnings. In other words, a shareholder is now an owner of the issuing company. Ownership is determined by the number of shares a person owns relative to the number of outstanding shares. For example, if a company has 1,000 shares of stock outstanding and one person owns 100 shares, that person would own and have claim to 10% of the company’s assets and earnings.

Mutual funds are a blend of stocks managed by a professional team or organization. There are hundreds of them and cover all types of diversification and topics. Some of the more popular companies are Vanguard and T. Rowe Price. They provide investors exposure to the market without having to manage the day to day events of individual stocks.

Benefits:

-Managed baskets of stocks by professionals.

-Lots of different categories.

-Published yearly and monthly returns.

Downsides:

-Fees can be very high and hidden.

-Sub-Par returns

-No control in how the funds distribute and allocate stock purchases.

Index Funds are a portfolio of stocks that match a particular stock index. For example, if you want to invest in the S&P 500, the easiest way is to buy an index fund like SPY. This fund tracks the S&P 500 and your return is based on the performance of the index, not the performance of a management time like in Mutual Funds.

Benefits of Index Funds

- They offer an easy way to “invest” in the market

- They typically have low fees

- They track indices that have historical returns.

Some Downsides of Index Funds

- They can experience a lot more volatility since they are based on a mix of many stocks.

- The way most indexes work is that they re-balance stocks in the index depending on performance. Because of this, an index fund can be overweight in stocks that are always at the top of their valuation vs. an underperforming stock that has value. The impact smooths out the growth.

How come REITS, Bonds, BDC, and other types of investments are not listed. Simple, these other investment types come with unique risks and require further research and much more explanation. If you are just getting started with investing, it is best to stay within investment options that are a bit easier to understand. Once you get the feel, you can branch out to get different kinds of investment returns.

So what investment type is right for you?

It really depends on your knowledge, time, and objectives. For example, if you are a set it and forget it person, then Mutual Funds and Index Funds are a great starting place because they allow strategies that are well defined and you can make your investment and not worry too much about managing it.

On the other hand, if you have time to research individual stocks, manage your portfolio at least weekly, and enjoy trading than individual stocks are a good option.

In most cases, the best option is a blended approach where you might have all three. The amount you invest in each option as mentioned before really depends on your time, commitment, and knowledge of trading.

Investment Objective

Understand the different types of investment offerings there are and what type of investor you want to be. Knowing this will help guide you to investments that match your style of investing.

Sart Investing: How to set up an Investment Account

Setting up an investment account is very similar to setting up a bank account. In fact, many investment account providers are also banks.

So what is the typical process? Most can be done online or if you have branches near you, they can be done in person. They will typically require money to fund the account, personal information (name, SS, DOB, etc.), and some disclosures about market risk and other information. Most will also ask your investment experience as this helps sets certain features on your account.

Other things to consider during the application process:

- Do you need to assign a beneficiary?

- Will your account be a joint account with a spouse or trusted person?

- Will your account be a retirement account (roth or traditional), a normal trading account, or some other special type of account.

The one thing that may be new to you, however, is the concept of Margin. Most accounts will offer this feature and it is something usually found in the sign-up process. Margin is the ability to borrow money against your investments to make additional investments within that account.

Account Fees

In comparing the different offerings, the first things you want to consider are the fees charged by the broker and bank. The fees for the accounts can be vastly different from broker to broker. It is important to know them and how they will impact your type of trading.

For example, brokers like Schwab offer a family of no-load (no fees) mutual funds. This gives you access to a great number of funds that Schwab will not charge you to invest into and the funds themselves are very low cost.

Here is a great comparison of the different pricing available from different brokers courtesy of Nerd Wallet.

The other thing when looking at pricing is also know how much the broker wants for a minimum deposit. They can range from $0 to $100,000. The higher balance firms usually offer more customized or personal service. The lower ones are typically self serve but have higher support offerings for a fee or percentage of your investment.

About Margin Accounts

- A margin Investment account allows you to borrow funds from the broker in order to leverage more funds for investments.

- A margin account allows for the purchase of other products offered by that broker (stocks, options, bonds, etc.)Margin uses leverage to increase the impact of certain investments and magnifies either the loss or profit of a trade.

- The amount of margin used is charged a fee by the broker.

- Using margin can be very risky and result in margin calls or account liquidation.

What Kind Of Investment Account to Open?

The great thing about investment accounts today is that there are dozens of different choices tailored to your style of investing. Not too long ago, investment accounts were complex, expensive, and required thousands of dollars. Now you can get ones that are free, quick to open, and as simple as clicking a button to auto-invest.

Deciding what type of investment account is best for your investing style depends on the goals you have, the amount of service you want, and the number of investment choices you desire.

There are so many, but most investment accounts can be broken down into several categories:

Large Institution Banking & Investment Account

Some of the players in this space are Fidelity and Merrill Lynch. They are investment brokers but also have banking services. In the case of Merrill Lynch, the banking services are tied to Bank of America. In these types of accounts, you can get the best of both worlds in one account login interface.

Pros

- Lots of services from investments to mortgages

- Typically have branches in most major cities

- Offer a kind of one shop stop for banking, investment, and lending.

Cons

- Higher fees typically

- Lack of personal service except for higher net worth individuals

- Not always flexible

Pure Trading Platforms or Discount Brokers

These types of brokers offering highly technical products that allow you to do research, chart overlays, and many other comparisons. They go way beyond the tools that you might see in Yahoo Finance and offer toolsets that range from technical stock screeners to option testing.

The brokers in this category typically target the power investor or the trader that wants full control. However, in recent years they are adding more and more services to target beginning investors. Some players in this space are etrade and tdameritrade.

Pros

- Lots of tools to research, analyze, and find target stocks

- Lower fees and account minimums.

- Easy order entry and quick trade execution.

Cons

- Not the full range of services link a larger institution.

- Lack of personal service except for higher net worth individuals.

- Some learning curve required to understand ordering.

Hybrid Investment Brokers

These types of brokers are a combination of the pricing and control of a discount broker with the services of a large broker. For example, Charles Schwab use to compete heavily in the discount broker market place but has since added banking, Robo advisory, and account maintenance. With a Schwab account, you get a lot of the benefits of a large Institution without the headache of dealing with a company like Bank of America.

Pros

- Lots of tools to research, analyze, and find target stocks

- Lower fees and account minimums.

- Easy order entry and quick trade execution.

- Banking and other personal services.

Cons

- Some of the add on features may not be as robust as a large institution.

- Options can be confusing.

- Some learning curve required to understand all the fees and account interactions.

Basket Investment Services

This one is newer to the market, but the idea behind firms offering these services is to give the account holder the ability to create a blend of stocks and only be charged one transaction fee. In a typical investment account, if you wanted a blend of 20 stocks, you would have to buy them all separately, assign the dollar amounts at the time of purchase, and pay fees for each of the trades.

With a basket broker, you pick your blend of stocks, the percent of the portfolio it should be, and then you make trades into your basket. The money you trade purchases shares of the stocks based on your percentages. In a way, it lets you create your own mutual fund.

Another great way these services are taking the market is by offering baskets based on themes. For example, you can buy a socially responsible basket that only contains companies that meet that definition. There are hundreds of choices and it creates a new and unique way for an individual to create a blended portfolio.

For an example basket investment service check out motif investing.

Pros

- Ability to create your own basket of stocks and automate investments into that basket

- Lower account and trading fees since it combines all purchases into one transaction

- Ease of managing a lot of stocks

Cons

- Limited choices of other products

- Not suited for individual stock investing

- Customer service

Drip and Sponsored Investment Accounts

These accounts are typically offered by mutual funds, corporations, or investment funds to offer automated investing into a single source investment or a single family of funds. They are typically managed by one of the larger investment firms but are labeled as the sponsor of the investment account. A way you might use and Drip account is to set one up with one of the major mutual fund companies and automate a few dollars a week to invest in the fund they are offering.

Pros

- Set it and forget

- Typically no fees

- Low minimum contributions

- Ideal for building an investment savings over a long period of time

Cons

- Limited choices of investments

- Accessing money takes time

- Not designed for active trading

Funding Your Account

Once you have found the right broker, submitted your paperwork, and selected your account type, the last thing you will need to do before making actual investments is funding your account.

There are three typical ways that you can fund your account:

- Via a wire or check sent to the institution per their instructions.

- Through Direct Deposit.

- Initiating a roll-over or transfer from another account.

Depending on what option you choose the process can take as little as a few days and as long as a few weeks. If you have any questions on how to fund your account, make sure to review that with your broker via a live call to ensure you know how long it is going to take and the correct procedure for each of the different options.

Beginning To Trade

Now that you have funded your account, you are ready to start trading. Depending on what type of account you have chosen, there are many different ways to begin trading. What to trade, how to trade, and strategies of trading will be left for future posts as there are thousands of books on those topics alone.

However, here are a few rules I follow to get you started

- Diversify as much as possible. In smaller accounts, full diversification may be difficult, but start small and add new positions that are different from your existing ones.

- Diversify investment types. I use a a few rules when I invest. The bulk of my investments are in safer investment types like index funds and mutual funds. I save a smaller investment amount for stocks and options.

- Don’t chase profits. If something has gone up over the past six months it does not mean it will continue. Do good research, invest in solid companies.

- The shorter your horizon the more risk you will have. Just like investing in one stock is risky, so is trying to make some quick money over a short amount of time. Sure, there are day traders that make tons of money, but they are the exception not the rule. They are also armed with experience, an understanding of markets they are trading in, and hopefully enough funds to whether ups and downs.

- Don’t be scared to take profits. Don’t take the point above to mean that you have to stay in a position even it has passed your target. Take your profits and move to other positions.

- My best results are when I limit my single positions to no more than $2,500 each. Why? Because it limits loses, forces diversification, and prevents me from buying into one stock to heavily. That number may be lower for you (or higher), the point is set a rough number and use it to make smart choices. I do have exceptions to this rule when it comes to some mutual funds and index funds that I don’t want to actively manage. They don’t typically carry the risk an individual stock can have and therefore I increase the amount before I diversify. My largest loses have come from investments where I broke my own rule.

- Dollar cost averaging is your friend. Small investment over time in solid market based funds or healthy dividend portfolios can average out the ups and downs over time.

I can’t stress enough, if you don’t have rules, don’t have a strategy, and don’t have time to manage your portfolio then limit your options to mutual funds, index funds, or other managed investment types. They are designed to be a low management investment to help you grow your portfolio with out the stress of managing individual stocks.

If you ignore that advice, then assume the money you are investing in the stocks without a strategy is like going to Vegas. Sure you may hit it big, but in the end the house usually wins.

Wrapping up your intro to investing

That is a lot of information to know and that is only just the surface. Here is the good news, there are lots of products out there in today’s market that allow investing to become a lot more automated and easy. However, it does not mean that you should not know at least the basics.

Investing can grow your portfolio and build wealth, it can also lose you all your money if done incorrectly. The most stable and solid approach for those not wanting to invest years of learning is a broad based market portfolio diversified across some different products. For example, a portfolio may include some index funds, a few sector focused mutual funds, a few individual stocks, and some bonds. There are even products out there that will make that exact mix.

For those just getting started, index funds are a great place to start as they are low cost, follow the broader market, and liquid.

Let’s summarize the key steps to getting you up and running

- Determine how much you can invest and what you can “afford” to lose.

- Determine what kind of investor you want to be. Set it and forget it, active trader, basket trader, etc.

- Research what feature you will need and what kind of broker fits your needs.

- Apply for an account.

- Fund your account.

- Set some rules, learn some trading concepts, and makes some of your first trades.

As an ending note, remember the importance of diversification. Here is a chart of sector based performance over time. It is hard to predict the winners and losers.